Three New Buildings Will Mean $1 Million More in Taxes Diverted to the DDA. What Is Going On?

Editor’s note: This special “follow the money” analysis by ELi relies on extensive longitudinal and investigative reporting. You can access sourcing through the hotlinks provided. Some of the hotlinks lead to a supplementary ELi article providing answers to readers’ questions related to this report.

The East Lansing Downtown Development Authority will soon see its revenue shoot up by about $1 million per year. The new funds will come chiefly from the diversion of local property taxes on the land of three new big downtown buildings: the new MSUFCU building, The Abbot apartment building and The Graduate Hotel.

ELi recently learned that, because of a tax-capture scheme set up years ago, by three years from now a total of nearly $1.9 million in downtown East Lansing property taxes that would otherwise be going to the City of East Lansing, Ingham County, Lansing Community College (LCC) and the CATA bus system will instead go into the East Lansing DDA’s coffers every year.

Unless something changes in the governance systems of East Lansing, the Council-appointed DDA members will have the power to decide what to do with all those taxpayer dollars.

Not lost on current DDA members is the fact the DDA still owes over $5 million on the bonds used to buy the Evergreen Avenue properties in 2009. While the principal on that debt has barely dropped in 14 years (because the DDA has consistently elected to spend its revenue on something other than principal payments), the DDA has now spent over $2 million in public money just on interest and fees related to those bonds.

All this time, the DDA has hoped a developer would solve its Evergreen bond debt problem by proposing a new development project for the properties and folding the debt into a project-specific financing scheme. But, as ELi recently reported, the latest proposal for the land just fell apart, like every proposal before it. The debt’s size has made redevelopment very difficult.

The coming influx of diverted new property taxes from the MSUFCU building, The Graduate and The Abbot could be used to pay off the Evergreen Avenue bond debt quite quickly, minimizing how much more public money is spent on interest and bond-related fees.

But now, as members of the DDA are talking about what to do with all the additional tax revenue that is about to divert to their authority, some on the DDA want to use most of the new funds not to pay off the debt fast but to hire more DDA staff and do more DDA special projects.

Regardless of what happens, it looks as if the DDA is poised to become a much bigger financial player in the governance of East Lansing. That could change only by an act of the City Council, and there’s no such action on the table.

From where does the DDA draw the $1.5 million it currently takes in every year?

The DDA obtains revenue from multiple sources. Chief among them is the DDA Special Millage, a Council-approved extra property tax on privately-owned land in the DDA district. That’s the area shown below in green.

The DDA Special Millage currently brings in about $270,000 per year. The income from that millage is going up fast as redevelopment downtown generates more and more taxable value. It is expected to almost double in five years, to a half-million dollars per year.

Until DDA members voted to knock down the buildings on the Evergreen properties, the DDA also had rental income of over $330,000 per year from those parcels. But that income, once used to pay interest on the bonds used to purchase the properties, is now mostly gone.

So, how is the DDA currently meeting its debt obligation while also paying for discretionary projects like Albert EL Fresco? Chiefly through tax revenue diversion.

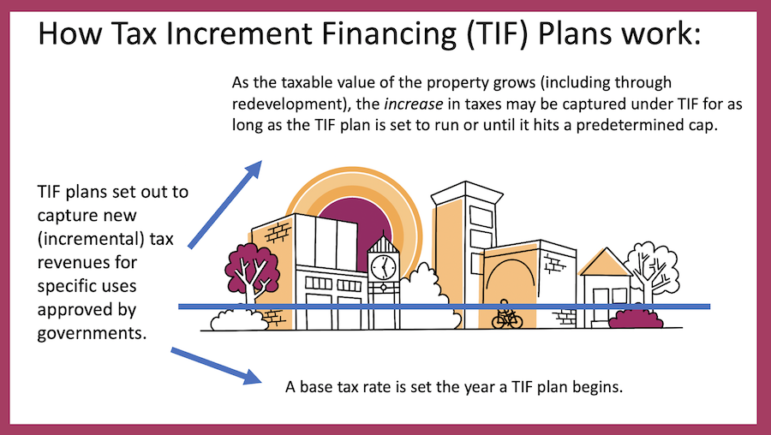

The DDA obtains diverted tax dollars through two Tax Increment Financing (TIF) plans, called DDA TIF #1 and DDA TIF #2. They are two different types of TIF, both allowed under state law and approved by the City Council and DDA.

In both cases, the approved plans capture and redirect property taxes that are generated each year above what was the initial base tax level. (That’s why it’s called tax increment financing.)

East Lansing’s DDA TIF #1 was created in 1986 for the University Place project, the complex that now houses the Marriott Hotel, retail and office space.

DDA TIF #1 is a Brownfield TIF plan. That’s the kind of TIF used to capture newly-generated property taxes from redeveloped land to support redevelopment of that land. In short, future taxes are pledged to help fund the redevelopment. The idea behind Brownfield TIF is to use carefully planned capture-and-diversion of tax revenue increases to spur redevelopment of contaminated or underperforming land.

Under DDA TIF #1, for a record-breaking total of 60 years, taxes have been and continue to be captured at the University Place (Marriott complex) development and redirected to the DDA’s accounts. The taxes redirected by DDA TIF #1 would otherwise flow to the City of East Lansing, the East Lansing Public Library, LCC, Ingham County and CATA.

The DDA doesn’t have discretion about how to spend the money coming in from TIF #1. The DDA is required to use all of the funds flowing in to pay for construction and maintenance costs of the underground city-owned parking garage at the Marriott complex off MAC Avenue.

The requirements of TIF #1 currently redirect about $136,000 in taxes per year through the DDA’s account to pay for that parking garage.

DDA TIF #2 is a different kind of TIF, sanctioned by Michigan state law to fund a broad array of DDA projects.

Under this TIF law, township boards and city councils can create special DDA TIF districts. Then, over the years, as taxable values rise on the DDA TIF-district properties, the DDA gets to capture the incremental increase in taxes.

East Lanisng’s DDA TIF #2 covers a geographically huge tax-diversion scheme. And it has no end-date. It will go on until the City Council decides to stop it.

Created in 1991 and expanded in 1997, DDA TIF #2 captures and diverts real estate taxes above the original base value from most properties in the DDA district west of Collingwood Drive.

Across this entire area (shown in yellow and orange in the map above), the DDA captures taxes that would otherwise be going to the City of East Lansing, LCC and CATA. In the orange part, the DDA is also capturing taxes that would otherwise go to Ingham County. (Ingham County “opted out of the 1997 expansion” of the DDA’s TIF #2 district, so the yellow area doesn’t include capture of county taxes.)

DDA TIF #2 is currently diverting about $853,000 per year in property taxes to the DDA.

But, because three recent big redevelopment projects are about to start having their incremental property taxes also diverted to the DDA, the DDA’s revenue from TIF #2 will soon go up by about $1 million per year.

Those three properties are the MSUFCU project, which is expected to be completed in 2023; The Graduate Hotel; and The Abbot apartments, next to The Graduate.

Completed in 2020 and 2021 respectively, The Abbot and The Graduate have already started producing large amounts of new tax money. But those incremental taxes have been getting captured for a Brownfield TIF to pay for project-related expenses, mostly new city infrastructure in the area.

The Brownfield TIF for The Graduate and the Abbot is finishing up much faster than anticipated. And that means soon – because of how DDA TIF #2 was set up by Council years ago – tax revenue from that land that would otherwise go to the City of East Lansing, LCC and CATA will instead be handed over to the DDA.

This means that the DDA’s revenue from TIF #2 is about to shoot up as taxes are diverted to it, away from the city, LCC and CATA. Here’s a snapshot of how key portions of the DDA’s revenue is changing:

City staff have not yet publicly broken down how much of this additional $1 million will be diverted from the city, LCC and CATA, so ELi is not able to give figures showing how much each of these taxing authorities are losing from DDA TIF #2’s tax diversion.

As more and more Brownfield TIF plans in the downtown finish, the DDA will be obtaining more and more new tax revenue.

To give you a sense of just how many properties we are talking about the DDA capturing taxes from, we’ve made a photographic montage. This shows buildings downtown that are currently subject to Brownfield TIF, i.e., tax capture to pay for the redevelopment of that land or nearby public infrastructure.

For all of these buildings, when the Brownfield TIF plans end, under DDA TIF #2, the DDA will then obtain the taxes that would otherwise go to the City of East Lansing, LCC and CATA. In some cases, the DDA is also going to be taking the tax revenue that would otherwise go to Ingham County.

The financial benefit of big new development to the DDA from TIF #2 came to light only relatively recently.

In the many public debates over downtown Brownfield TIFs that ELi has covered over the last eight years, no one ever seemed to mention that if downtown properties at issue didn’t have a Brownfield TIF, they’d instead be subject to a tax-capture by the DDA through TIF #2.

For example, in 2014, citizens sharply objected to a Brownfield TIF for 300 Grand (then known as “The Gateway”), and Council split 3-2 on the matter, granting the TIF. Everyone involved seemed to think they were debating Brownfield TIF or no TIF – not a Brownfield tax-capture versus a DDA tax-capture.

That included Councilmember Ruth Beier, an economist, who clearly thought a majority “no” vote on that Brownfield TIF would mean the taxes would go to the city instead of the developer. As she worried about the city’s pension debt, Beier presented to Council a calculation of how much the city’s general fund would supposedly be losing to that Brownfield TIF.

But as it turns out, if there had been no Brownfield TIF on 300 Grand/The Gateway, the DDA, and not the city’s general fund, would have been getting the city’s taxes. When the Brownfield ends, unless Council changes the TIF plan, the DDA will get the city’s taxes, along with LCC’s and CATA’s from that property.

Flash forward six years from that TIF approval to 2020, when voters were asked to approve the sale of a parking lot to MSUFCU for its big new building and city leaders talked about the big new property taxes the project would produce. A review of public hearings and publications from that time shows no record of city leaders or staff explaining that, because of DDA TIF #2, it would be the DDA, not the city’s general fund, that would receive those big new property taxes.

Similarly, when Council approved plans and the development agreement for The Abbot and The Graduate, there was no public discussion of the fact that when the Brownfield TIF on those properties ended, the DDA would immediately take over capturing East Lansing’s property tax revenue from those properties. Again, in voting yes on the TIF, Beier believed the taxes would ultimately benefit the city’s pensions.

By contrast, the HUB at Bogue Street and Grand River Avenue is not in the DDA’s TIF #2 tax capture area and has had no big Brownfield TIF. That property is now generating almost $1.8 million a year in property taxes, including about a million going just to the City of East Lansing.

With none of the HUB’s tax revenue redirected to the DDA, City staff have seen the HUB property as a major new revenue source that is helping address East Lansing’s troubled pension debt.

But the HUB is a big exception. In most of the core downtown, it’s been developers and the DDA, not primarily the city’s general fund, benefiting from the growth of taxable value through TIFs.

That means it is chiefly homeowners around the city paying for citywide services like police, fire, road repair and the like as the big commercial properties pay instead for their own redevelopment and for the DDA.

Homeowners all over the city are subsidizing public services to the downtown. And that’s set to continue indefinitely under TIF #2. It won’t change unless a majority of Council acts to change it.

Plans for the DDA’s upcoming revenue surge are up in the air.

At the DDA’s meeting on Nov. 17, presented with the projected surge of funds, DDA member Jeff Smith calculated the DDA could use the money to hire four to five full-time staff in the coming years.

Following Smith, City Manager George Lahanas (a member of the DDA by virtue of his office) floated the idea of creating a new “Downtown Division” like the Parks & Rec Department in the City of East Lansing. He suggested it could have a dedicated supervisor and staff focused on downtown, with their own trucks and other equipment.

Lahanas said the new diverted tax revenue could also “allow [the DDA] to put more money into the Project Development Fund.” That’s the fund the DDA has been using to pay for special projects like façade improvements on private businesses downtown, public art projects, sidewalk repairs, security cameras and the Albert EL Fresco entertainment area.

Those are all projects the DDA has elected to fund instead of paying off the Evergreen Avenue property debt.

Soon, the DDA will have to use at least some of the TIF #2 revenue for paying the Evergreen debt.

That’s because of two things: the Evergreen properties are no longer producing six-figure annual rental income since the buildings were vacated and demolished, and the Evergreen properties’ bonds pledge DDA TIF #2 revenue as security.

That said, instead of paying that debt off quickly with the surge of incoming diverted taxes, with Council’s consent the DDA may decide to stretch the Evergreen properties debt out for another two decades or more.

Stretching out the refinancing bonds would shrink the annual payments required on the bonds. While this would result in far more interest paid from taxes in the long run, it would give the DDA a bigger annual cash flow to do what it wants in the short-term.

And at least some DDA members, including Lahanas, appeared at the Nov. 17 meeting to be interested in that approach.

Council will be asked on Dec. 13 to approve the third refinancing bond for the DDA’s Evergreen properties debt since 2009. City staff has not responded yet to questions from ELi about how long the new bonds are proposed to run.

If it’s a short period, that will mean the DDA must use its money to meet its debt obligation sooner. If it’s a long period, the DDA will control a lot more discretionary funding, giving the DDA members more power to shape East Lansing in the coming years.

Appreciate ELi’s reporting and want to see it continue? Then make a tax-deductible contribution today to help ELi continue its work into 2023. We can only do this work with readers’ financial support.